AI in Insurance Underwriting: Smarter Risk Assessment, Faster Decisions

Introduction

Insurance underwriting has always been about weighing risk against reward. But the old way? It is painfully slow. Manual data collection eats up days. Risk scores rely on thin information. And good customers end up waiting far too long for a simple yes or no.

AI in insurance underwriting flips the script.

What once took weeks now happens in hours or minutes. Data drives decisions, not gut feelings. Frustrated customers turn into happy policyholders who actually stick around.

This guide walks you through what AI insurance underwriting really means, how it works under the hood, and how your organization can start using it today to write better business faster.

What Is AI in Insurance Underwriting?

AI in insurance underwriting means using artificial intelligence to evaluate risk, set premiums, and decide whether to accept or reject applications. Simple enough.

Traditional underwriting? That is human judgment based on a small handful of data points. Credit scores. Medical history. Driving records. The applicant fills out forms. The underwriter reviews them. Done.

Artificial intelligence underwriting does the same job but on a completely different scale. It pulls data from dozens of sources automatically. It finds patterns human eyes will never catch. It makes consistent, data driven decisions in real time. And here is the kicker: it learns. Every single application makes the system smarter about what good risk looks like.

Why AI in Insurance Underwriting Is Gaining Importance

The insurance market is more competitive than ever. According to Accenture, insurers anticipate AI adoption in underwriting will increase from 14% today to 70% in the next three years.

- Customers want instant quotes. They shop around online. If one carrier takes three days to respond, they have already bought from someone else.

- Underwriters are drowning. Manual reviews take hours per application. Complex cases take even longer. Carriers simply cannot scale their teams fast enough to keep up with demand.

- Regulators are watching too. They want consistent, fair underwriting decisions. Artificial intelligence insurance underwriting delivers exactly that when implemented correctly.

AI for insurance underwriting solves both sides of this equation. Speed climbs. Workload drops. Accuracy improves across the board.

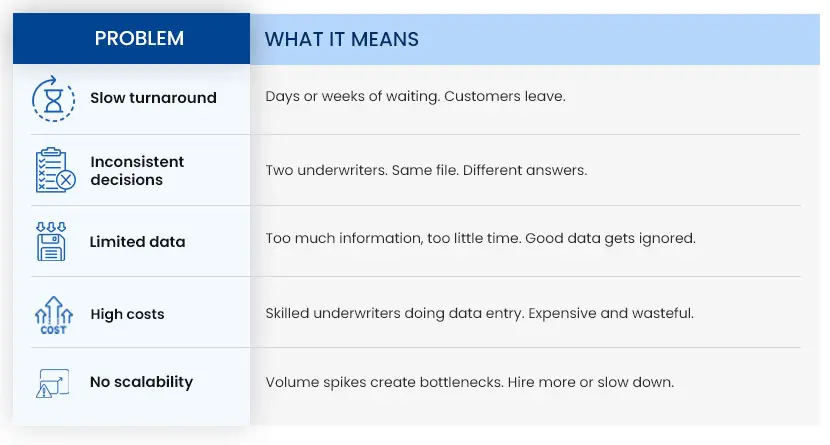

Limitations of Traditional Underwriting Processes

Traditional underwriting has some real problems. Here is what AI in insurance underwriting fixes.

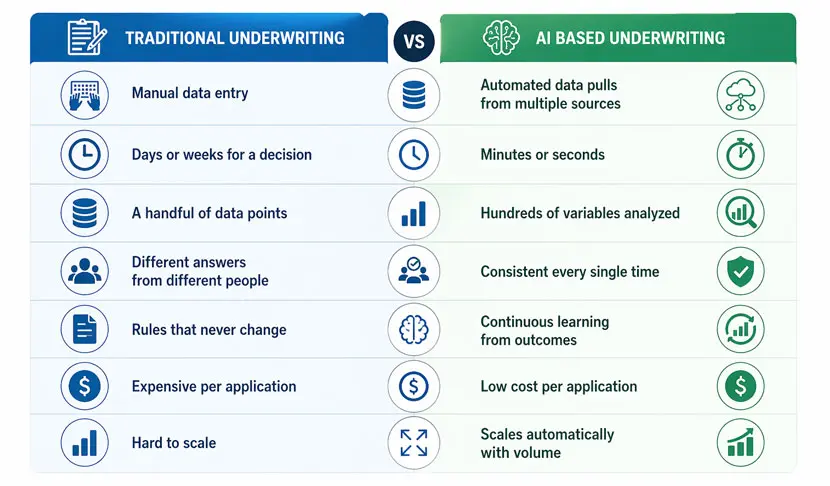

Traditional vs AI Based Underwriting

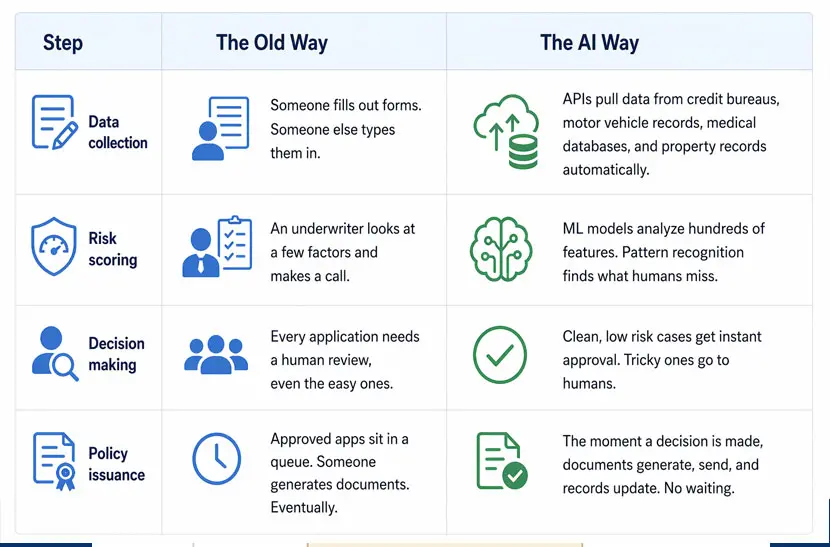

How AI Is Transforming Insurance Underwriting

AI in insurance underwriting changes every step of the workflow, from the moment data comes in to the moment the policy goes out.

Key Benefits of AI in Insurance Underwriting

Organizations that adopt AI in insurance underwriting see real results. Databricks found that AI powered underwriting systems process applications 70% faster while maintaining accuracy.

- Faster turnaround. Decisions go from days to minute. Customers get answers instantly.

- Lower costs. Automation handles routine work. Underwriters focus on cases where they add value.

- Better risk selection. AI finds good risks that old methods would reject and bad risks that might slip through.

- Consistent decisions. No more variance between underwriters. Same standards. Every time.

- Happier customers. Fast and fair decisions make people renew. Simple as that.

- Scales like crazy. Application volume doubles? The AI does not break a sweat. No hiring spree required.

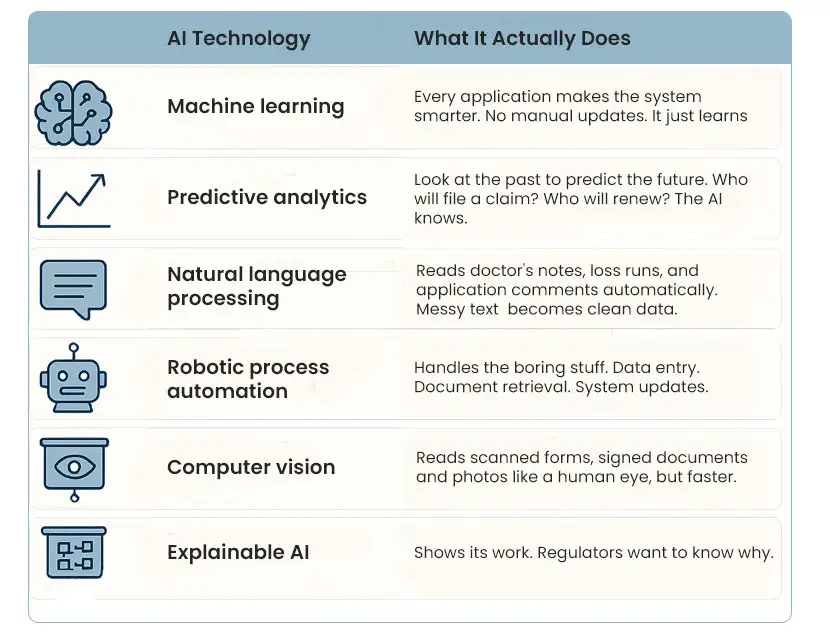

Core Technologies Behind AI in Insurance Underwriting

Several technologies work together to make AI insurance underwriting possible. Here is what is happening under the hood.

Real World Use Cases of AI in Insurance Underwriting

AI in insurance underwriting works across every major line of business.

- Life insurance underwriting- Traditional life underwriting means medical exams, blood work, and weeks of waiting. AI changes that. The system pulls prescription history, electronic health records, and motor vehicle reports. Many applicants get approved instantly. No needles required.

- Health insurance risk assessment- Health underwriters look at medical history, lifestyle factors, and expected utilization. The AI processes claims records, pharmacy data and wearable device information. A complete risk profile in seconds.

- Property and casualty underwriting- P&C means property characteristics, location risks, and loss history. AI pulls from public records, satellite imagery, and prior claims databases. It assesses wildfire risk, flood risk, crime statistics, and more. All at once.

- Auto insurance underwriting- Auto underwriting looks at driving records, vehicle type, and usage patterns. AI adds telematics data, credit based insurance scores, and where permitted, other signals. The result is a precise, fair risk assessment.

- Fraud detection using AI in insurance underwriting-Fraud often starts at the application. False information. Stolen identities. Inflated asset values. AI flags all of it before policies are ever issued. Carriers avoid losses before they happen.

Challenges in Implementing AI in Insurance Underwriting

Implementing AI in insurance underwriting comes with real hurdles. Knowing them upfront helps carriers plan better.

- Data quality. AI needs clean, complete data. Messy data in means bad decisions out. No way around it.

- Legacy systems. Many carriers still run on outdated policy systems that store data in silos. Getting them to talk to modern AI takes work.

- Regulatory compliance. Underwriting algorithms cannot discriminate unfairly. Models need to be explainable and auditable. Black boxes do not fly here.

- Talent gaps. Carriers need people who understand both insurance and AI. That combination is rare and expensive.

- Change management. Underwriters worry AI will replace them. Clear communication about AI as a tool, not a replacement, makes all the difference.

How to Choose the Right AI Solution for Insurance Underwriting

Not every AI for insurance underwriting solution delivers the same results. Here is what to look for.

- Insurance specific training. General purpose AI misses industry nuances. Choose a solution built for underwriting.

- Easy integration. The AI should connect to your existing systems without a massive, expensive tech project.

- Explainable decisions. Regulators will ask why. The system must provide clear answers.

- Customizable models. Every carrier has a unique risk appetite. The AI should adapt to your rules, not the other way around.

- Proven results. Ask for case studies and references from similar carriers.

- Strong security. SOC 2 certification, data encryption, and regulatory compliance.

Best Practices for Implementing AI in Underwriting

- Start with a pilot. Pick one product line or one underwriting team. Prove value. Then expand.

- Keep humans in the loop. AI handles routine cases. Underwriters handle complex or borderline cases. Together they are stronger.

- Monitor continuously. Track approval rates, loss ratios, and customer outcomes. Watch for unintended bias.

- Train your team. Underwriters need to hone Agentic workflows and how to override it when necessary.

- Document everything. Regulators will ask for model governance, validation results, and decision logs. Have them ready.

Will AI Replace Insurance Underwriters?

No. AI will not replace underwriters. It will make them better. Think of AI as a powerful assistant. It handles data collection. It runs calculations. It flags anomalies. It approves simple cases.

But complex risks? Those still need human judgment. Unique situations need human empathy. Relationships with brokers need human connection. Underwriters who use AI in insurance underwriting will outperform those who do not. The role shifts from data entry and manual review to exception handling, strategy, and relationship management.

Future Trends in AI in Insurance Underwriting

The future of AI in insurance underwriting looks exciting.

- Real time underwriting. Customers will get binding quotes in seconds for almost every product.

- Continuous underwriting. Policies will update automatically as risk profiles change. Add a teenage driver? Premium adjusts instantly.

- Personalized pricing. Usage based and behavior-based insurance that rewards good risk management.

- Agentic underwriting. AI agents will not just recommend decisions. They will execute end to end workflows, only escalating exceptions to humans.

Conclusion: Making AI Work for Insurance Underwriting

AI technology helps insurance companies achieve quicker decision-making processes which reduce operational expenses while improving their capacity to evaluate risks and maintain uniform results to satisfy their clients. The key is choosing the right solution and implementing it thoughtfully. Start with a small project which demonstrates value before you proceed to expand your operations. Beyond Key can help you take that first step.

Beyond Key: Your AI Underwriting Partner

We deploy AI agents for:

- Intelligent Document Processing

- Fraud detection

- Automated risk assessment

- Case summarization

- Workflow automation